By Alexander McDonald, Senior Director of Lending Operations

For communities to thrive, they need resources — but too often, small business owners, developers, and local community development leaders lack access to the capital they need to drive progress.

Across the Momentus Capital branded family of organizations we are on a mission to change that through a community-first approach to lending grounded in our commitment to diversity, equity, and inclusion. And for us, that includes much more than the actual continuum of capital we deliver, but also HOW engage with our borrowers and partners to do that. Every aspect of our lending operations is built on our values, which means taking out a loan from Momentus is a much different experience than borrowing from a traditional financial institution.

But our approach doesn’t just feel good. It also leads to exceptional outcomes. The secret to our success? Putting the borrower first with superior client service, competitive products, and scaffolded support.

And our lending operations team is at the heart of what makes Momentus unique.

To learn more about how our lending operations team works with borrowers and supports social impact, please read our full blog on the Momentus Capital website.

By Masouda Omar, Head of Small Business & Community Development Credit – Lending Operation

As a Community Development Financial Institution (CDFI), Capital Impact Partners has played a part in both upholding and dismantling systemic racial bias in the credit system.

Since our inception, we have served sectors, industries, and borrowers not served by the traditional financial system.

Like many CDFIs, Capital Impact provides more flexibility than traditional lenders in some key areas like loan-to-value limits and financial covenants that borrowers must meet.

However, our credit guidelines – the policies that guide our loan structures and lending decisions – are built on the traditional approach to credit that has deep roots in a financial system that intentionally excluded people of color for much of its history. Often, our lending team seeks one or several “exceptions” to our credit guidelines to accommodate the diverse needs of our diverse borrowers.

Creating flexible financing is both a mindset and an approach. To do so, we need input from our clients and communities to rethink and reshape our products and requirements. When done correctly, this approach gears us away from the extractive patterns of traditional financing and closer to confirming that when people are given the opportunity to succeed, their communities, local residents, and our country thrive.

At Momentus Capital, we envision a future where everyone has the capital and opportunities they deserve – especially those who have been excluded from both for so long.

Our President and CEO Ellis Carr reflected on the contrast between Independence Day celebrations and a set of Supreme Court decisions that challenged promises about democracy, opportunity, and the pursuit of happiness.

His reflections tackle a few areas:

How promises about democracy, opportunity, and the pursuit of happiness have been shaken;

How these decisions will have negative consequences on fellow citizens who have faced long decades of discrimination; and

Momentus’ commitment to continue to speak and work in support of underestimated communities.

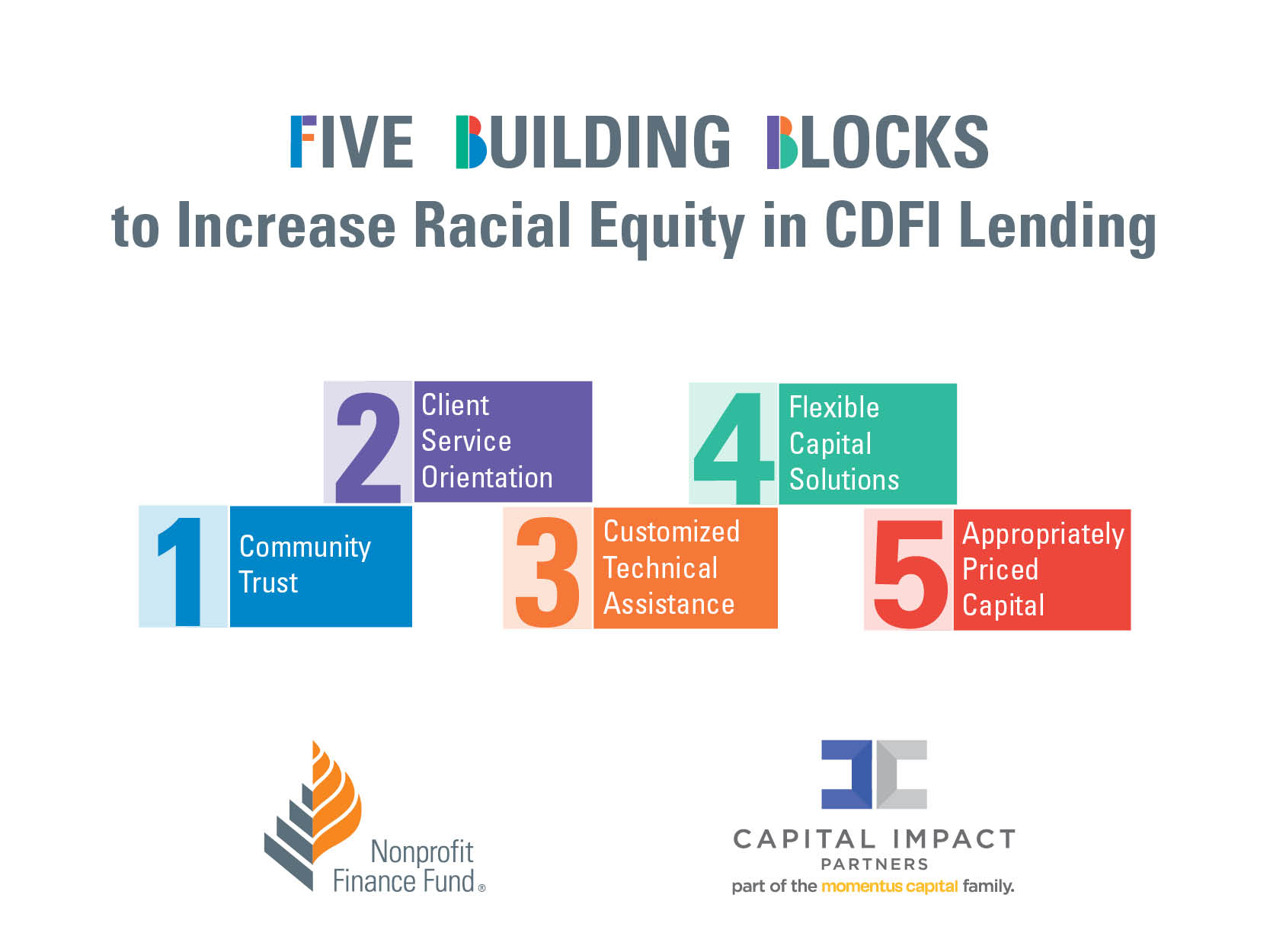

Community Development Financial Institutions (CDFIs) were born out of the civil rights movement to ensure that nonprofits and businesses — particularly those in communities of color and communities with lower incomes — have equitable access to loans. Yet, CDFIs are part of a financial system embedded with discriminatory lending practices which need to collectively be addressed in order to fully achieve the intended goal of equalizing access to financial resources for all people.

Momentus Capital’s family of organizations, including Capital Impact Partners, CDC Small Business Finance, and Ventures Lending Technologies, is working to help support economic mobility and wealth creation through more equitable access to capital for communities that have been long overlooked by traditional financial organizations.

In line with this commitment, and in recognition of discriminatory lending practices identified within CDFIs, Capital Impact Partners collaborated with Nonprofit Finance Fund (NFF) to identify and address policies and practices that contribute to it. We conducted research to understand how some local and national CDFIs have successfully taken steps to address inequity within their own lending practices.

Learn more about the partnership and read the full report here.

Affordable housing development firms led by people of color – both nonprofit and for-profit – are highly underrepresented in the housing industry, yet are a critical resource for strengthening the housing development ecosystem as a whole and expanding the supply of homes that are affordable. Currently, people of color are estimated to make up less than 5% of the developers in the country.

To support the growth of and opportunities for developers of color in the Washington metro area, as well as increasing the amount of affordable housing regionally, Capital Impact Partners partnered with Amazon to create our Housing Equity Accelerator Fellowship (HEAF). The fellowship provides training, mentorship, and grant capital to support wealth building for developers and their firms, and community building through increased affordable housing.

One of our HEAF participants is Ronette “Ronnie” Slamin, founder of Embolden Real Estate. In this blog profile by HAND, she discusses her journey to becoming a real estate developer, how she views real estate development as a tool to address infrastructure issues, and being intentional about creating space for women and people of color.

As the first quarter of 2023 unfolds, Momentus Capital team members are starting to see trends for an exciting year ahead. And while 2022 proved to be another rollercoaster ride for the economy and small businesses, our experts still forecast plenty of opportunities to make 2023 a groundbreaking year in mission-based lending.

In this year’s predictions, we take a deep dive into a wide range of topics, including how communities can lead the way to greater economic prosperity, how we can get more capital into the hands of small businesses, and potential legislative changes on the horizon. Ultimately, we remain focused on how these factors could impact our borrowers, partners, investors, and the communities we serve. This valuable foresight serves as a compass for existing entrepreneurs and those embarking on their ventures.

Please read the rest of this blog on the Momentus Capital website.

At Momentus Capital, we believe that residents from all walks of life should have equitable access to the things that contribute to their health and wealth. This is especially vital for underestimated communities that often have a harder time accessing resources like good jobs, affordable housing, accessible health care, and more. When these things are present in communities, local and global economies become more prosperous and resilient.

Our CEO Ellis Carr recently spoke about building community resilience at the Yale School of Management (SOM)’s Economic Development Symposium. This annual student-run conference brings together senior thought leaders, practitioners, and investors from academia, government, NGOs, and the private sector to discuss the latest issues in economic development.

His speech tackled a few areas:

The history of law and policies that have deliberately excluded communities of color;

Where we stand today in terms of health and wealth disparities, despite signs of progress; and

A vision for the future including things that the public sector, private sector, and individuals can do together to support the growth of healthy, inclusive, equitable, and resilient communities.

Please read the rest of this blog on the Momentus Capital website.

It’s Black History Month! This month, we will celebrate by illuminating the social and economic experiences that shape the lives of African American communities. We also wanted to take a moment to share the history of Black History Month and the theme for this year.

Did you know that Black History is a tradition that started in the Jim Crow era and was officially recognized in 1976 as part of the nation’s bicentennial celebrations? It aims to honor the contributions that African Americans have made and to acknowledge their sacrifices. Each year, the Association for the Study of African American Life and History (ASALH) chooses a different theme, with this year’s theme focusing on “Black Resistance.”

As a real estate developer looking to deliver social impact, the process of finding and engaging with a lender can be hard. Once your mind is set on starting a community development real estate project, who do you turn to? Where do you find them? What is the process like?

As part of the Momentus Capital family of mission-driven lenders, Capital Impact Partners – a certified Community Development Financial Institution (CDFI) – provides flexible and affordable loans of $650,000+ ($350,000 under special circumstances) to finance key community pillars, including health centers, education facilities, food retailers, affordable housing, small businesses, and cooperatives.

We are a national lender, capable of providing loans across the country, but we also have a place-based focus in specific regions, including California, Michigan and northwest Ohio, the New York Tri-State Area, the Southeast, Texas, and the Washington metropolitan area.

We know you have got questions about the community development real estate process. To help get your process started, we offer some answers here about working with a CDFI lender.

1. When in the development process should I start working with a CDFI lender?

It is never too early to start gathering information from lenders, but you’d ideally want to get started when you are about six months from starting construction.

By then, you would have a good estimate for the timing of obtaining permits and starting construction.

CDFIs such as Capital Impact Partners will work hand in hand with real estate developers looking to deliver social impact

2. What types of reserves will a CDFI lender require?

Lenders will have contingencies on your project that may go above and beyond what you have budgeted; usually 7.5-15% of hard costs expenses and 5% of soft cost expenses.

If you are capitalizing interest during construction, which is recommended when there are no operations ongoing during construction, that will need to be included in the overall project budget.

Once construction is completed, there may be lease up reserves, debt service reserves, and/or facility maintenance reserves.

3. Where does the capital that CDFIs lend come from?

CDFIs serve as capital aggregators that attract capital from the market, banks, government sources, and foundations.

4. Will a CDFI lender hold the loans or will they sell them?

CDFIs do both. At Capital Impact, if they are sold, we ensure that there is no impact on the Borrower’s experience or relationship.

5. What influences CDFI lenders’ rates?

Primarily it is the Treasury rates, unless the CDFI has a sector/geographic fund that is independent of Treasuries.

6. Who approves the loan and how does the loan committee work?

CDFIs have groups that review deals. Capital Impact has an internal credit committee that reviews deals on a weekly basis.

Some CDFIs or specific loan products require external review and approval. Underwriting packages must be submitted at least a week in advance to receive approval the following week.

The committee cares about the financial strength of the transaction, the deal fitting into our established credit guidelines, and the impact of the transaction on the community.

8. Who will be my main contact for loan closing and will it change afterwards?

You may first interact with a business development officer or someone with a similar position, who will be the initial point of contact until a term sheet is signed.

Then you’ll speak with a loan officer who will underwrite your transaction until it is approved.

Once approved, a legal and closing team will drive the process, but the loan officer will remain involved to ensure the loan is closed according to what was agreed to with the borrower and as outlined in their underwriting.

9. As a non-legal person, how do I review a loan agreement?

Consider seeking legal counsel to review a loan document. But generally, check that the interest rate, fees, and dates match your understanding. Check the reporting and financial covenants to ensure you can meet them.

10. What should I do if I think I am going to default on my loan?

Tell your lender as quickly as possible. CDFIs are lenders with a mission to provide fair, responsible financing, and they will work closely with you when things are tough. Another very important element to take into consideration when looking to establish a relationship with a community development real estate lender is that lender’s value system. You have the right and responsibility to vet the lender to make sure that their values, goals, and philosophies align with yours. It is a two way street and any conversation about funding should be as much about the entrepreneur evaluating the funder as the funder evaluating the entrepreneur.

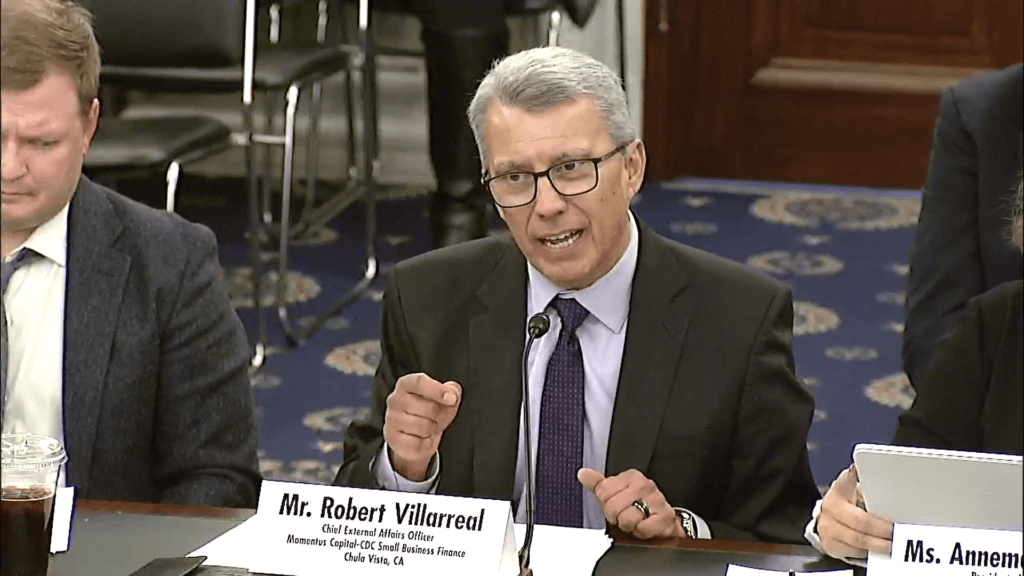

Momentus Capital’s Chief of External Affairs, Robert Villarreal, recently testified in front of the Senate Committee on Small Business and Entrepreneurship about improving access to capital in disinvested communities through the Small Business Administration (SBA) Community Advantage (CA) loan program.

The Community Advantage pilot program was launched in 2011 to expand the points of access that small business owners had for getting loans from mission-driven financial institutions. These lenders intentionally support underestimated community members, businesses, and organizations – with an emphasis on assisting people of color, women-owned businesses, and startups.